How to Manage the Pitfalls of the Shared Vacation Home

Key Takeaways:

- Family Property Can Create Conflict Over Time — What starts as a fun, shared gathering place can cause tension as more family members get involved. If there is no clear plan, disagreements about money, usage, and decisions will arise.

- An LLC Helps Organize and Manage the Property — Putting the property into an LLC gives the family a clear structure because it defines who manages what, how decisions are made, and how ownership changes are handled. This makes things fairer and less emotional.

- Planning Ahead Is Essential for Long-Term Harmony —To keep the property and family relationships strong, families need to talk openly, make rules, and write things down. Without a plan, problems will grow as the family grows.

The Problem

Looking back, Sam, Jane, and Nick’s childhood seemed nearly perfect. They grew up in a loving family, played sports year-round, and traveled frequently. But the highlight for the three siblings was always the summer weeks spent at Manor Grove, the family’s vacation home on the Outer Banks, bought by their grandparents in the 1960s.

When their grandparents passed away, the house went to their father, James, and his sister, Clara. As the years rolled by, Manor Grove remained the family’s anchor. But as Sam, Jane, Nick, and their cousins married and had children, the logistics of sharing the property became increasingly complex. Disputes between James and Clara over use and upkeep morphed from occasional friction to regular conflict. After a particularly nasty fight ten years ago over renovating the kitchen, James bought Clara out. They haven’t spoken since.

When James died last year, ownership passed to Sam, Jane, and Nick. Although the siblings remain close, they are already feeling the strain the property is causing in their relationships. Just this past year, Jane installed new curtains ($20,000) without consulting her brothers, who balked at the cost. Sam, who lives on the West Coast, believes he should have priority to use the house over the July 4th weekend because he rarely gets to use it.

Above all, the three siblings want to preserve their relationship. Unlike their dad and his sister, they don’t want this special property to become a wedge that drives them apart. They hope the property will bring their families together, not divide them. Yet dividing the use of the property and sharing the rising costs fairly are creating friction.

The good news? By identifying issues early and establishing clear ownership and governance, a shared vacation property can be a blessing rather than a burden.

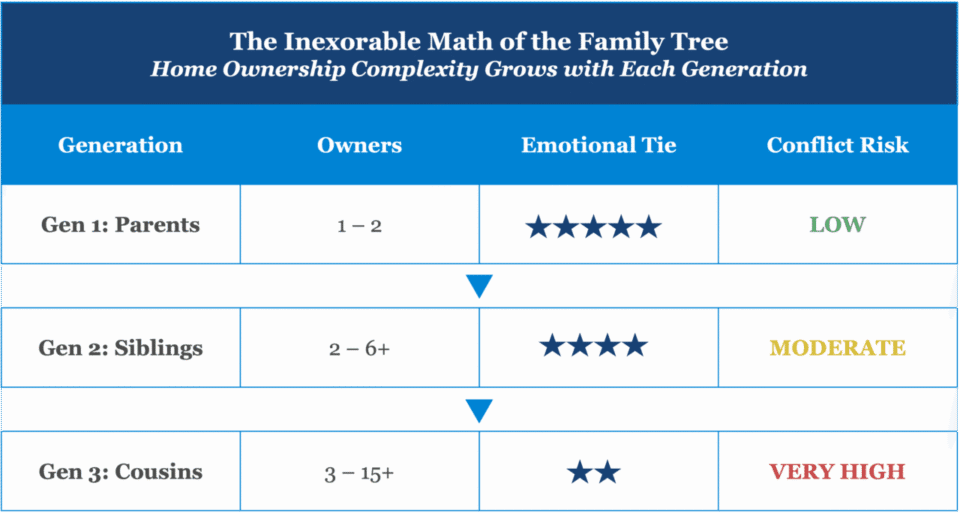

The Inexorable Math of the Family Tree

The Manor Grove story illustrates a common risk of shared family wealth: what brings families together in one generation can tear them apart in the next. The problem isn’t just emotional; it stems from the math of the family tree. Consider the typical progression:

Generation One: Mom and Dad own the property. They make decisions, pay the bills, and determine its use. Friction is kept in check by parental authority.

Generation Two: The children assume ownership. Now, siblings (and potentially spouses) must reach consensus on everything. Disagreements become more common.

Generation Three: By this stage, there are usually ten or more descendants (cousins) and their spouses. Consensus is almost impossible.

by Generation 3. Structure and governance are essential to bridge this gap.

Beyond the numbers, the relationship dynamics shift. Generation Two consists of siblings who share childhood memories, grew up under the same roof, and know each other’s triggers and tendencies (for better or worse). But Generation Three? These cousins may barely know each other. They were raised apart, with different values, financial situations, and memories of the property. While siblings might fight like cats and dogs but ultimately reconcile at Thanksgiving, cousins lack that shared foundation.

Plus, emotional attachment tends to fade over time. If your parents built the beach house, your attachment to it is strong because of the summers and holidays you spent there. If your great-grandfather built it and you visit once or twice a year, your connection is weaker. This variation in emotional investment directly affects family members’ willingness to contribute financially and their satisfaction with ownership.

Three Foundational Issues

Whether it’s siblings or distant cousins, three foundational issues often undermine the harmonious ownership of vacation homes. Anticipating them will help you address them in advance.

1. Financial Disparity

As families grow, financial circumstances diverge. One sibling might be an investment banker; the other, a school teacher. The banker may view a $30,000 annual assessment as a minor expense, while the teacher sees it as a significant burden.

Families with vacation homes often inherit wealth passed down through generations. While inherited money can cover property expenses, it also adds complexity. If Jane has one child, Sam has two, and Nick has three, their equal inheritance from their parents creates a significant disparity in the next generation. Jane’s child receives a full one-third interest, while Sam’s child receives one-sixth, and Nick’s children each receive one-ninth. By the fourth generation, some second cousins will have multiple times as much family wealth as others. This widening gap in inherited wealth makes it harder to maintain broad willingness to own the home and contribute financially.

One way to address this issue is to endow the property (i.e., set money aside in an account for property maintenance and capital expenses). The advantages and disadvantages of this strategy are discussed in the solutions section below.

2. The Calendar Wars

For a beach house, everyone wants the Fourth of July. For a ski condo, everyone wants the week after Christmas and President’s Day. As families grow and more people compete for these peak times, the property starts to feel like a timeshare, except you can’t blame a faceless corporation when you end up with a rain-soaked week in October.

Geography complicates this further. If one sibling lives an hour away and uses the house every open weekend, while the others live across the country and visit only once a year, tension is unavoidable. The local sibling argues that her siblings have the same access she does and that it’s not her fault they chose to live far away. Her siblings see it differently: they can only get to the condo on holidays, while she can use it all the time, so they should get the prime dates. Both perspectives are valid.

3. The Funding Dilemma

Vacation real estate, by virtue of being in a desirable destination, is expensive to own. Property taxes tend to be high, insurance can be substantial (especially in areas prone to hurricanes or wildfires), and maintenance costs tend to fall in the category of “you’ve got to be kidding me.” Add in utilities, landscaping, cleaning, and seasonal opening and closing, and the annual tab can be substantial.

The central question is how family members share that burden: based on ownership percentage or on amount of usage?

- Ownership-Based: The ownership-percentage approach has the virtue of simplicity. If you own 25 percent, you pay 25 percent of the costs, regardless of whether you spent three months or three days at the house. But this can breed resentment when usage varies widely. Why should a family member who rarely visits subsidize the heavy users? The heavy user, of course, sees it differently. Those who rarely visit have every opportunity to come more often, and their choice not to shouldn’t financially penalize those who do.

- Usage-Based: The usage-based approach, which allocates costs based on the number of days used, appeals to a different sense of fairness, one that aligns costs with benefits. But it creates a potential “death spiral.” Charging for usage discourages visits. As usage drops, the cost-per-visit rises, further discouraging use. Eventually, the house sits empty, and most owners want to sell.

A possible solution is to use a hybrid model like fractional airplane ownership: owners pay an annual fee based on their ownership percentage, which covers most of the cost, along with a pay-per-use rental fee.

Solutions: Structure Before Emotion

Families who successfully maintain properties across generations treat the property less like a clubhouse and more like a business. They establish structures that prevent emotions or disagreements from destroying relationships.

The LLC: Depersonalizing Decisions

While the technical details of Limited Liability Companies (“LLC”) can fill pages, here’s what matters: an LLC separates ownership from management and creates clear decision-making processes. An LLC’s governing document, called an operating agreement, designates the LLC’s “managers” and specifies which decisions require approval by the owners, who are called “members.”

Managers handle the day-to-day:

- Paying bills

- Scheduling repairs, upkeep, and improvements under a set dollar amount

- Recommending capital improvements to the Members for approval

- Managing the property usage calendar

- Hiring contractors and repairmen

Members vote on or approve material items which commonly include:

- Major capital improvements and maintenance costs over a set dollar amount

- Approving annual budgets

- Adding or removing managers

- Sale of the property

- Rules for property usage and transfers

- Changing the rules/agreement

The LLC operating agreement doesn’t address every issue up front. Instead, it provides a process for making decisions. It shifts decisions from the emotional realm (“Mom would have wanted…”) to the procedural (“The operating agreement says…”).

While a property can be placed in an LLC at any time, the more owners there are, the harder it will be to get everyone to agree. Thus, the best time to place a property in an LLC is during generation one.

The Endowment Option: Solving the Cash Flow Crunch?

One specific tool to address the financial disparity mentioned earlier is to endow the property. In this scenario, the generation passing down the home also leaves a sum of money designated to cover the property’s ongoing costs. While this can be a powerful tool, it also presents challenges that families must carefully evaluate.

The Pros: The main advantage is that it addresses the immediate cash flow issue. If the “house account” covers taxes, insurance, and maintenance, the sibling with modest income isn’t forced to stretch their budget. It keeps the property as a retreat rather than a financial burden.

The Cons: An endowment is not a magic bullet, and it comes with two primary issues:

- The Sticker Shock: It requires a massive amount of upfront capital. For a vacation home with $200,000 in annual carrying costs, you would need to set aside nearly $5 million to permanently endow it. Even a substantial $2 million fund would likely be depleted in less than 15 years.

- The “Pot of Gold” Problem: Endowing the property doesn’t make costs disappear; it just capitalizes them. Future owners will look at the endowment fund and realize that if they sell the house, they don’t just receive their share of the real estate—they also split the remaining millions in the endowment. This can inadvertently increase the pressure to sell, as the opportunity cost of keeping the house becomes a tangible, liquid fortune in an investment account.

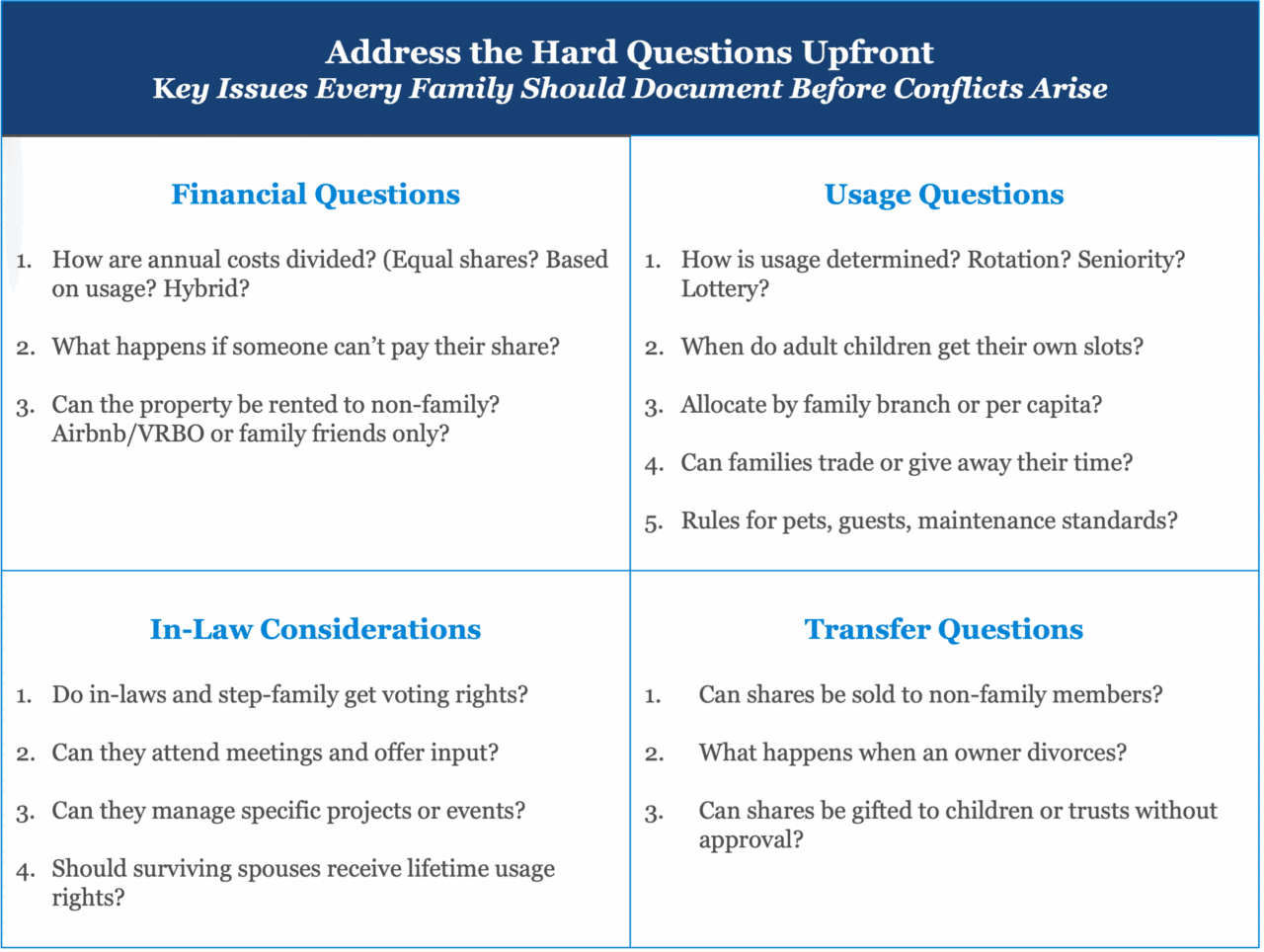

Address the Hard Questions Upfront

The best time to establish rules for potentially contentious issues is before you need them. The answers to some of the questions below should be included in the LLC’s operating agreement, while others should be documented as resolutions by the managers or members. Your attorney or wealth advisor can advise on where and how to address these issues. Every family sharing property should document answers to the following questions.

on where and how to address each issue.

The Exit Strategy

The best time to establish rules for potentially contentious issues is before you need them. The answers to some of the questions below should be included in the LLC’s operating agreement, while others should be documented as resolutions by the managers or members. Your attorney or wealth advisor can advise on where and how to address these issues. Every family sharing property should document answers to the following questions.

Perhaps the most critical provision for family harmony is determining how an owner can leave. A family member who feels “trapped”—forced to fund a property they neither use nor can afford—is a recipe for discord.

However, you cannot simply allow anyone to cash out at full market value whenever they want; that could force a sale of the entire property to pay them off. The solution is a structured buyout mechanism in the Operating Agreement:

The Terms: The buyout is paid over time (e.g., via a promissory note over 5–10 years) rather than as a lump sum. This protects the remaining family members’ cash flow while providing a guaranteed path to liquidity for the exiting member.

The Right to Sell: A member can sell their interest, but the LLC (or other members) has the right or the obligation to buy.

The Price: The buyout price is usually set at a discount (often 20%-40%) of the appraised value. This discourages frivolous exits and acknowledges that a fractional interest in a private family home is worth less than the whole.

Making It Work: Practical Governance

Legal documents are the skeleton; governance is the muscle. Here is how to make it work in practice:

- Over-Communicate: Communication conveys respect. Create a property-specific email group. Hold an annual “State of the House” video call to discuss budgets and capital projects. Schedule additional update/communication calls as needed when important decisions are being made. Even if family members/owners don’t have a say in a decision, they should still be looped in on what’s going on.

- The “Boast Book”: Keep a log where family members record what they did during their stay—repairs completed and supplies purchased. It fosters friendly accountability.

- Plan for Change: What works for three siblings won’t work for twelve cousins. Build evolution into your agreements:

- Review the operating agreement every five years

- Rotate management responsibilities

- Transparency: Nothing breeds suspicion like financial opacity. Share detailed budgets. Use property management software to track expenses and calendar slots.

- Involve the Next Generation: Including younger family members in governance—even in small ways—builds their connection to the property. They might manage the property’s social media, organize cousin weekends, or handle technology upgrades.

- Explicitly Delineate Roles & Responsibilities: Property management shouldn’t rest on just one person. Nor should it be a free-for-all with no set responsibilities. Who is responsible for what needs to be clearly delineated. Roles such as who manages the usage calendar (based on the agreed-upon allocation rules) and who oversees repairs and maintenance.

When to Let Go

Sometimes the bravest decision is recognizing when shared ownership no longer serves the family. Signs it might be time:

- The property causes more conflicts than connections

- Maintenance costs exceed emotional value for most owners

- The next generation has little to no interest in ownership

- Geographic dispersion makes sharing impractical

- One or two family members would happily buy out the others

There’s no shame in selling to preserve relationships. Better to share memories of wonderful summers than to let a property destroy family bonds.

The Bottom Line

Shared family vacation properties are paradoxes—they are both sources of family fun and places to build treasured memories, and potential sources of deep division. The families who navigate this successfully don’t rely on love alone. They rely on systems.

The goal isn’t to remove emotion from these special places. It’s to create a framework that protects both the asset and the relationships it was meant to nurture. Because in the end, the memories made at Manor Grove matter more than Manor Grove itself.