When Everyone Gives Up: How a Magazine Article Signaled the Turning Point for Non-U.S. Stocks

Key Takeaways:

- Extreme Consensus Often Signals a Turning Point – When a major publication like The Economist publicly questioned the case for non-U.S. stocks, it reflected peak pessimism. This is historically the kind of sentiment exhaustion that precedes a reversal rather than continued decline.

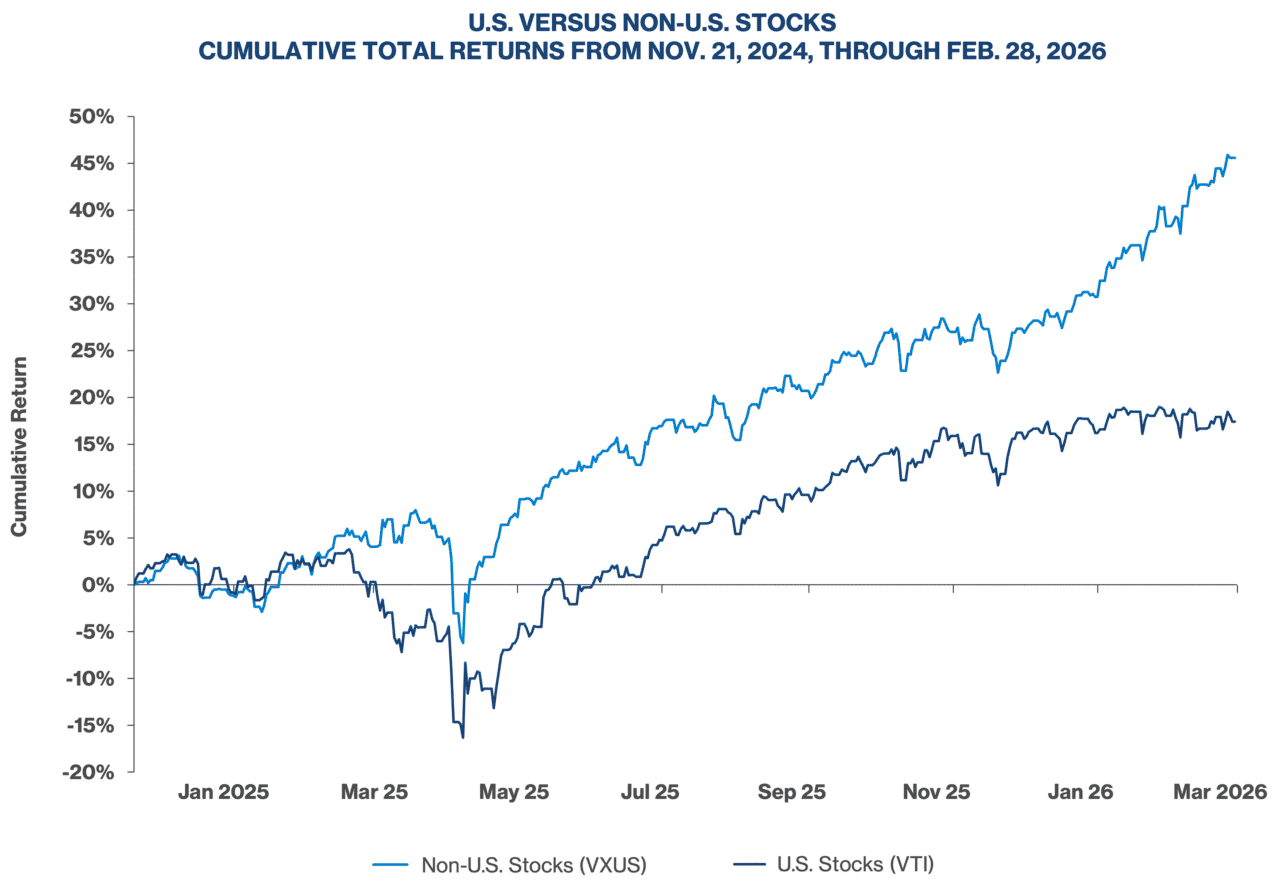

- The Rebound in International Equities Was Swift and Significant – Following the article’s publication, the Vanguard Total International Stock Index (VXUS) dramatically outperformed its U.S. counterpart, underscoring how deeply out-of-favor asset classes can surge once selling pressure is spent.

- Diversification Feels Uncomfortable Before it Pays Off – After 15 years of relative underperformance, non-U.S. stocks were cheap, unloved, and widely abandoned. This reminds investors that maintaining global exposure often works best precisely when it feels hardest to justify.

On November 21, 2024, The Economist published an article titled “Should Investors Just Give Up on Stocks Outside America?” For anyone familiar with the so-called magazine indicator – the idea that mainstream publications have a knack for capturing the consensus opinion at precisely the moment it’s about to reverse – this was a compelling signal: a widely read publication codifying the view that non-U.S. equities were a lost cause at the very moment that collective view might be most vulnerable.

From that date through February 2026, the Vanguard Total International Stock Index (VXUS) posted a 46% cumulative total return, trouncing the Vanguard Total U.S. Stock Index’s (VTI) gain by roughly 28 percentage points.

The magazine indicator isn’t mystical. It’s explainable by regression to the mean and consensus fatigue: by the time a narrative is entrenched enough to earn a prominent spot in a magazine (whether it be a cover story or a featured one), every investor who is going to act on that view already has. What’s left is a reversal. The pattern has been formally studied: A 2016 Citigroup analysis examined 44 Economist covers with a strong directional view on an asset class and found they were contrarian roughly 68% of the time over the following year.

History offers some vivid examples. In August 1979, BusinessWeek published “The Death of Equities” with the Dow near 800 after a miserable decade of stagnant returns. Within a few years, stocks launched into one of the greatest bull runs in history. Two decades later, The Economist’s March 1999 cover declared the world was “Drowning in Oil” with crude just above $10 a barrel. Oil began a historic ascent that peaked near $147 in 2008.

The Economist’s late 2024 issues offered a small cluster of these signals beyond the international stocks article. “The Everything Drugs,” published on October 26, 2024, chronicled how Novo Nordisk’s Ozempic and Wegovy would reshape healthcare. Novo’s stock has since fallen from around $113 to roughly $38 as of February 2026. “America’s Gambling Frenzy,” published on December 5, 2024, coincided with a period during which DraftKings’ shares declined more than 40%. Counterarguments spring to mind—Eli Lilly has fared far better than Novo since the drugs cover, and casino operator Las Vegas Sands has held up despite other gambling stocks languishing. Individual stocks have too many idiosyncratic drivers for a magazine column to be a reliable single-stock signal.

But the international stocks article was different. It wasn’t a call on a single company or sector. It captured the collective exhaustion of a decade and a half of relative underperformance. That’s where the indicator tends to work best: not as a stock-picking tool, but as a barometer of positioning at the asset-class level.

Why did international stocks reverse so sharply? There’s no shortage of catalysts one can point to in hindsight: A weakening dollar (which helped translate foreign returns back into more attractive U.S.-based results), fiscal stimulus across Germany and parts of Europe, surging demand for South Korean memory manufacturers amid the AI buildout, and Japanese Prime Minister Sanae Takaichi’s landslide election victory and the promise of pro-growth policies for the world’s fourth-largest economy.

Perhaps the simpler explanation is that the setup was just right. Non-U.S. stocks had suffered through 15 years of lackluster returns relative to their American counterparts. They were cheap by most valuation measures, unloved by investors clamoring for the returns of U.S. large caps, and—as The Economist article made plain—consensus had fully capitulated. When everyone has already given up, there’s no one left to sell.

Taking a contrarian position is more of a complement than a core component of an investment strategy, and it can certainly get you into trouble if taken to extremes. But for a globally diversified portfolio—which endured a long winter of being weighed down by its non-U.S. constituents—the reversal has been significant. There’s an investing adage that says, “if you don’t hate part of your portfolio, you’re not properly diversified.” Non-U.S. stocks gave investors plenty to hate for 15 years. It’s a reminder that diversification often feels the worst right before it starts working again.