The Financialization of Bitcoin

Key Takeaways:

- Bitcoin Has Become Increasingly Correlated with U.S. Equities as it Has Matured –What began as a niche, thinly traded asset with wildly fluctuating correlations has evolved into one that consistently moves alongside the Nasdaq 100 and S&P 500, weakening its diversification appeal.

- Institutional Adoption and Financial Products Have Driven This Shift – The launch of futures, ETFs, and corporate treasury allocations integrated Bitcoin into mainstream portfolios, making it more sensitive to macro forces like liquidity, monetary policy, and overall risk sentiment.

- Greater Accessibility Has Come at the Cost of Independence – Like commodities in the 2000s, Bitcoin’s financialization has tethered it more tightly to traditional markets, suggesting it may fall in tandem with equities during major downturns rather than act as a reliable hedge.

How It’s Getting Harder to Make the Case for Bitcoin as a Portfolio Diversifier

Over the past several years, Bitcoin has increasingly traded like a risk asset alongside U.S. stocks, namely the Nasdaq 100 and S&P 500. As it has moved from a fringe novelty to an institutionalized financial asset, its co-movement with U.S. equities has become less episodic and more persistent, reducing the reliability of diversification benefits.

That evolution mirrors what occurred in commodities in the 2000s: The proliferation of, and massive flows into, commodity-linked products diminished the assets’ once-beneficial diversifying features. For example, a 2013 London Business School study found that institutional inflows into commodity futures drove prices well beyond what fundamentals justified. This financialization unmoored the asset class from supply and demand, a process now mirroring Bitcoin’s trajectory.

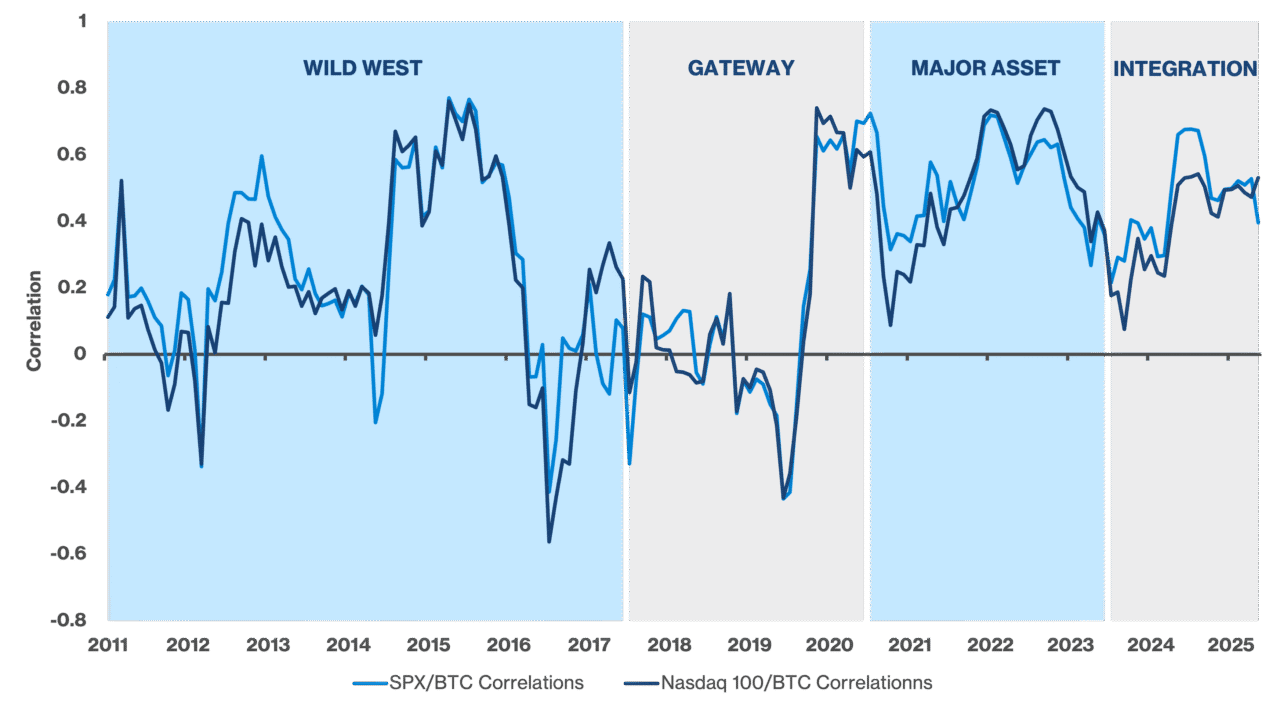

The four shaded regimes in the accompanying exhibit A trace this shift, linking each stage of market maturation to the observed behavior of rolling 12-month correlations.

Exhibit A: Bitcoin’s Rolling 12-Month Correlation With U.S. Equities

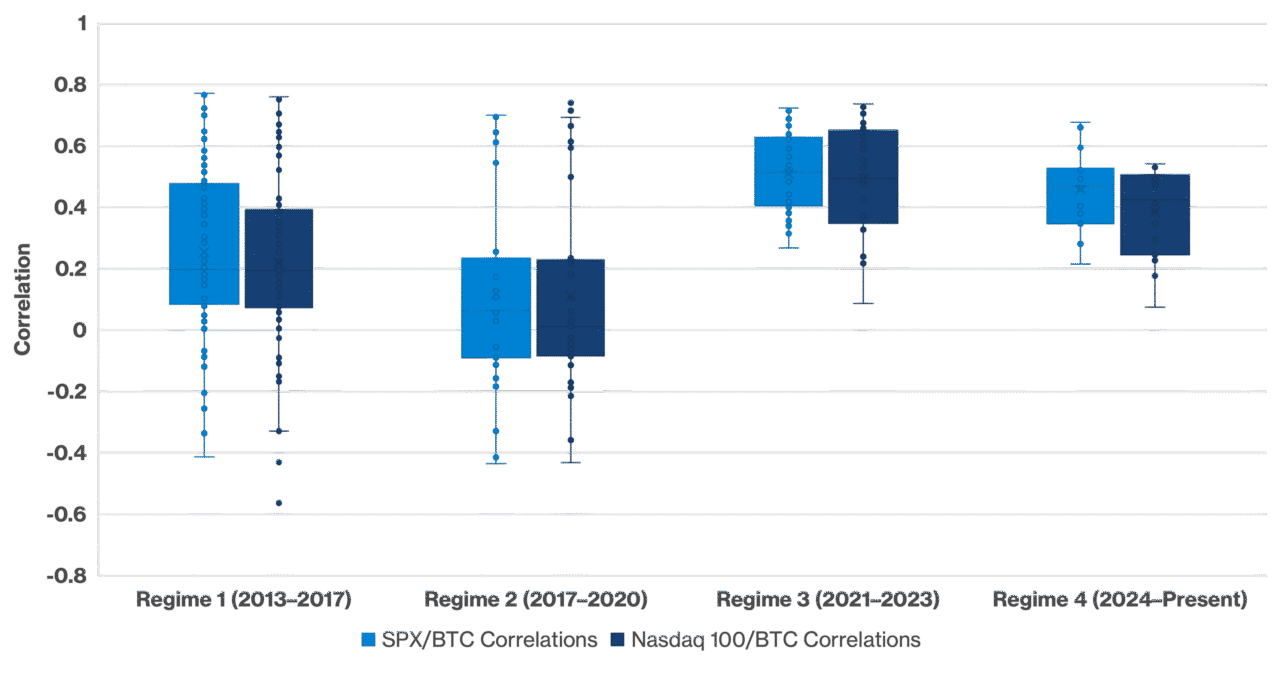

While Exhibit A highlights how correlations fluctuated over time, Exhibit B reframes the same data bucketed by regime, showing that co-movement has become less dispersed and more directionally similar, reflected in a higher median correlation and a tighter distribution in the post-2020 periods.

Exhibit B: Bitcoin’s Equity Correlations Have Become More Persistent

Regime 1 (2013 – 2017): Wild West

During this period, Bitcoin existed, but far from the mainstream. While the U.S. Financial Crimes Enforcement Network (“FinCEN”) issued compliance guidance in 2013, legally recognizing the asset, it remained, functionally, a niche form of currency used on dark web platforms. Trading venues were fragmented, liquidity was thin, and institutional participation was nonexistent. Correlations with equity markets oscillated wildly (ranging from -0.6 to 0.8) and had little fundamental connection to equity markets, as Bitcoin was not widely held in the same portfolios or influenced by the same market forces as traditional assets.

This resembles the pre-index (i.e., pre-2000) era in broad-based commodities: smaller markets, local drivers, and minimal integration with global financial flows.

Regime 2 (2017 – 2020): Gateway

The late 2017 launch of Bitcoin futures by the Chicago Mercantile Exchange (“CME”) and Chicago Board Options Exchange (“Cboe”) was the first real bridge to Wall Street. Institutions could speculate, hedge, and build systematic strategies without handling the underlying asset. This brought Bitcoin a step closer to mainstream financial markets.

In 2020, MicroStrategy and Square (now Block) added Bitcoin to their balance sheets, reframing it as a corporate-treasury reserve asset. These events pulled Bitcoin further into institutional workflows, contributing to a gradual uptick in correlations as ownership broadened and price behavior became more sensitive to global liquidity conditions.

This was analogous to the mid-2000s rise of commodity index traders, where giant institutional pools of capital began to outweigh bona fide hedgers (producers and consumers) and traditional speculators.

Regime 3 (2021 – 2023): Major Asset

Coming out of the COVID pandemic, Bitcoin’s market cap surpassed $1 trillion in early 2021, placing it squarely on the radar of global macro investors. El Salvador’s adoption of Bitcoin as legal tender wasn’t necessarily a watershed moment, but it prodded central banks and governments to seriously engage with digital assets.

The launch of the first U.S. Bitcoin futures ETF (BITO) in late 2021 dramatically expanded retail and brokerage-platform access, and Bitcoin-adjacent products such as Grayscale Bitcoin Trust (GBTC) garnered massive inflows.

As the Federal Reserve began tightening in 2022, correlations—which had increased during the COVID pandemic to average 0.6 from an average of -0.4—remained elevated: Bitcoin’s price moved in tandem with high-flying technology stocks, responding directly to movements in real yields, changes in the market’s liquidity expectations, and so-called risk sentiment.

Again, this is like the period of the mid-to-late 2000s when commodity ETFs such as SPDR Gold Shares (GLD), United States Oil Fund (USO), and United States Natural Gas Fund (UNG) launched and scaled, and commodities began to co-move with equities during risk-on and risk-off cycles.

Regime 4 (2024 – Present): Integration

The approval of spot Bitcoin ETFs in 2024 bolstered the link between crypto and traditional finance. These products enabled direct exposure through standard brokerage accounts, model portfolios, and advisory platforms. Trading volumes are increasingly concentrated in U.S. market hours, and flows into vehicles such as BlackRock’s IBIT ETF—among the fastest-growing in history—pulled Bitcoin deeper into equity-like behavior.

Correlations in this period are structurally higher because Bitcoin now participates in the same flow-of-funds dynamics, risk-management models, and macro narratives as the Nasdaq and S&P 500.

What Does This Mean for Bitcoin?

It doesn’t change what the asset is, but it does change how it behaves.

Consider the lesson of 2008: Whereas commodities had previously behaved differently from stocks in recessions, when the financial crisis hit, oil fell from $140 to $40, and broad commodity indexes got clobbered alongside the equity market collapse.

As with commodities, financialization has made Bitcoin more accessible—but also more correlated. While unique crypto-specific factors still matter, institutional allocation patterns, monetary policy expectations, and global liquidity are now among the dominant forces.

While the next major equity drawdown will provide another real test of whether Bitcoin moves against the grain or falls in tandem with stocks, its recent behavior shows an asset that increasingly trades with the market rather than apart from it. For everyday investors, the implications are straightforward: Bitcoin may still have strategic merit for potential growth, but including it in a portfolio for diversification benefits is a hard sell.