Why Jurisdiction Matters

Key Takeaways:

- Missouri is a Top-Tier Trust Jurisdiction Despite Being Overlooked – While advisors tend to default to well-known states like South Dakota, Nevada, and Delaware, Missouri offers a legal framework that is just as strong on the core metrics that matter. The gap between “headline states” and Missouri is largely reputational, not substantive, meaning advisors may be missing a highly competitive option simply because it’s less marketed.

- Missouri Matches or Exceeds Peers Across the “Three Pillars” – The state performs at or near the top in all three key areas of trust planning: perpetual duration, effective zero state income tax, and strong asset protection. The key insight is that Missouri’s “grantor-focused” tax label is misleading—in practice, many trusts end up paying no state income tax, making it functionally similar to no-tax states.

- The Biggest Barrier is Perception, Not Law – Missouri’s relative obscurity comes down to timing and marketing, not capability. Earlier movers like South Dakota built strong industry ecosystems and brand recognition, while Missouri didn’t promote its advantages as aggressively. Combined with a common misunderstanding of its tax rules, this has kept it off advisors’ shortlists.

Ask a roomful of estate planning attorneys to name the best states for trust situs, and you’ll hear the same answers within seconds: South Dakota. Nevada. Delaware. Maybe Alaska if someone’s feeling adventurous.

These jurisdictions have earned their reputations. South Dakota was first to abolish the Rule Against Perpetuities back in 1983, and its trust industry has been marketing that head start ever since. Nevada followed with aggressive asset protection statutes. Delaware built its brand on business-friendly courts and corporate trust infrastructure.

But here’s the thing most advisors don’t stop to examine: the actual legal gap between these “headline states” and other attractive jurisdictions is far narrower than the reputation gap suggests. And one state in particular, Missouri, offers a trust framework that competes head-to-head with the usual suspects on every metric that matters, while flying almost entirely under the national radar.

Estate planning attorney Steve Oshins publishes annual rankings of states for dynasty trusts and domestic asset protection trusts (DAPTs). His analysis, along with similar analyses from the American College of Trust and Estate Council (ACTEC) and Trusts & Estates magazine, is highly influential for good reason: they provide a structured framework for comparing state laws across the variables that matter most. Missouri ranks highly on these lists due to its long history of progressive, trust-friendly statutes. Yet when advisors consider attractive trust situs, Missouri is rarely mentioned..

That disconnect deserves a closer look.

The Three Pillars: Missouri’s Framework Compared

Advisors evaluate trust jurisdictions on three primary factors:

- How long a trust can exist,

- Whether trust income is subject to state taxation, and

- How effectively the trust protects assets from creditors.

Missouri performs at or near the top on all three:

Let’s explore each of these categories in more depth.

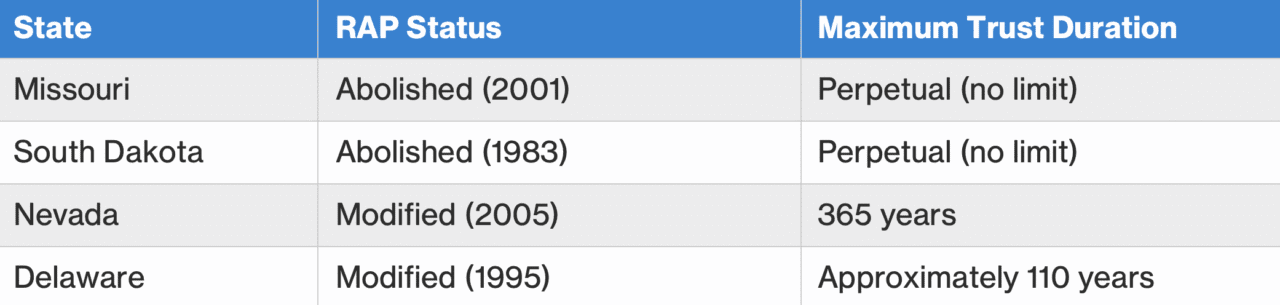

Perpetual Trust Duration

The Rule Against Perpetuities (RAP) is the old common law rule that historically prevented trusts from lasting more than roughly 21 years after the death of the last surviving beneficiary alive at the trust’s creation (usually 80–110 years in practice). For families pursuing multigenerational wealth transfer, this is a non-starter; it forces distributions and triggers estate tax exposure when the trust terminates at the end of the RAP.

Missouri abolished the RAP effective August 28, 2001, under RSMo § 456.025. Missouri trusts created on or after that date can exist in perpetuity: no expiration date, no forced termination, and no asterisks.

This is a meaningful distinction. Not every “trust-friendly” state offers true perpetuity:

For any family establishing a dynasty trust, Missouri’s perpetual duration stands on equal footing with South Dakota and exceeds what Delaware and Nevada permit. That’s not a minor technicality; it’s a foundational requirement for multigenerational wealth transfer planning.

Fiduciary Income Tax

This is where the biggest misconception lives. On most comparison charts, states fall into broad categories: “no income tax,” “grantor-focused,” “trustee-focused,” and so on. Missouri lands in the “grantor-focused” column, which at first glance looks less favorable than South Dakota, Nevada, or Alaska, all of which sit in the “no income tax” column by virtue of having no state income tax at all.

But the chart doesn’t tell the full story. Missouri’s fiduciary income tax only applies when both of the following conditions are met: the trust was created by a grantor domiciled in Missouri at the time the trust became irrevocable, and at least one income beneficiary is a Missouri resident on the last day of the taxable year. If either condition is absent, Missouri imposes no fiduciary income tax on any type of income. In practice, this means Missouri functions as a zero-tax jurisdiction for the vast majority of trust planning scenarios involving out-of-state families. Consider a straightforward example: a New York family establishes an irrevocable trust, names a Missouri-based corporate trustee, and the beneficiaries remain in New York. Because the grantor is not a Missouri resident, the trust owes zero Missouri fiduciary income tax while simultaneously avoiding New York’s 10.9% rate because the trustee (and thus the trust’s administration) is outside New York’s reach. On a $20 million trust portfolio of publicly-traded securities generating a 5% average annual yield, that’s roughly $135k per year in state income tax savings, compounding to well over a million dollars within a decade.

What about Missouri families? Would they be better off domiciling their trusts in a state like South Dakota or Nevada because of Missouri’s income tax? No. That’s because if a trust has a Missouri resident grantor and at least one Missouri resident beneficiary, it will be subject to Missouri income tax regardless of the trustee’s location, even if they are located in a no-tax state.

The bottom line is that Missouri isn’t a “no income tax” state in the bright-line sense, but for planning purposes, the practical outcome is identical. The general advisor pool sees Missouri outside the no-tax column and moves on. That’s a costly shortcut.

Asset Protection

Missouri ranks fourth nationally in the Oshins DAPT State Rankings for domestic asset protection trusts, behind only Nevada, South Dakota, and Ohio. The state’s statutory framework, codified primarily in RSMo § 456.5-505, permits a grantor to establish an irrevocable trust, retain a discretionary beneficial interest, and shield trust assets from future creditors, a combination that only 19 states currently allow. Plus, here’s a little-known fact: Missouri passed the nation’s first domestic asset protection trust law in 1987.

Missouri’s creditor protection framework is also notably strong for trusts that are not DAPTs. A spendthrift provision in an irrevocable trust will generally prevent the settlor’s creditors from satisfying claims against trust assets, except in cases of fraudulent conveyance or for alimony and child support obligations within a defined statutory window. Beyond that window, Missouri provides comprehensive asset protection from all creditor classes for any beneficiary of the trust.

This is an increasingly important consideration. The cost of liability insurance continues to rise, the litigation environment remains aggressive, and asset protection planning has shifted from a “nice to have” to a core component of comprehensive wealth structuring. Missouri’s top-tier standing in this area is a significant yet underappreciated advantage.

Beyond the Three Pillars

A state’s trust framework is more than just the Rule Against Perpetuities, taxes, and asset protection. The operational flexibility built into a state’s trust code matters enormously for long-term administration, and Missouri delivers here as well.

Missouri adopted and customized the Uniform Trust Code in 2005, providing a modern, comprehensive statutory framework for trust administration. Several provisions stand out:

- The state’s decanting statute (RSMo § 456.4-419, most recently updated in 2022) allows a trustee with discretionary distribution authority to transfer trust assets into a new trust with updated terms without court approval. This is an essential tool for modernizing outdated trust language, a need that becomes more pressing as trusts from the mid-20th century age into their third and fourth generations.

- Missouri also permits directed trusts (RSMo § 456.8-808), allowing the separation of investment, distribution, and administrative responsibilities among different fiduciaries, enabling families to retain investment control while relying on a corporate trustee for administrative and distribution decisions.

- Missouri law explicitly provides for trust protectors, a framework that offers additional flexibility by authorizing a designated individual to modify trust terms, change the trust’s situs, correct drafting errors, and adjust to changes in tax law.

- The 2025 legislative session saw four new Missouri Bar-initiated trust provisions pass the General Assembly, addressing trust situs transfers, statutes of limitations for trustee claims, electronic estate planning, and emergency planning procedures. This responsive legislative culture is a meaningful signal that Missouri continues to invest in its trust infrastructure rather than resting on existing law.

Why Missouri Gets Overlooked

If the legal framework is this competitive, why isn’t Missouri on every advisor’s shortlist?

Part of it is the first-mover effect. South Dakota abolished the RAP in 1983, nearly two decades before Missouri did. During those years, South Dakota’s trust industry grew, aggressively marketed, and established national referral networks. Delaware had a similar head start on the corporate trust side. By the time Missouri’s statutes caught up, the conversation had already been framed. Notably, Missouri’s trust companies did not market the state’s DAPT statute.

Another aspect is the competitive dynamics within the trustee market. South Dakota has a concentration of trust companies that actively compete for out-of-state business, creating a self-reinforcing marketing ecosystem.

Finally, there’s the mistaken perception about income tax. When an advisor scans a comparison chart and sees Missouri in the “grantor-focused” column rather than the “no income tax” column, the analysis often stops there. The nuance that Missouri’s tax regime effectively produces a zero-tax result for most out-of-state families is never examined. That single misperception may be the biggest obstacle to Missouri receiving the recognition its trust laws warrant.

Missouri: A Jurisdiction Worth a Second Look

Trust situs selection is one of those decisions that compounds quietly over decades, for better or worse. Families and their advisors who limit the analysis to a handful of well-marketed jurisdictions may be leaving meaningful advantages on the table. Missouri’s trust framework ranks among the strongest in the country by any objective measure, and its combination of perpetual duration, favorable tax treatment, and robust asset protection warrants serious consideration in any situs evaluation. Sometimes the best answer isn’t the most obvious one.

References

1. RSMo § 456.025, Inapplicability of the Rule Against Perpetuities (effective August 28, 2001). https://revisor.mo.gov/main/OneSection.aspx?section=456.025

2. RSMo § 456.5-505, Creditor’s Claim Against Settlor. https://revisor.mo.gov/main/OneSection.aspx?section=456.5-505

3. RSMo § 456.4-419, Trust Decanting Statute (updated 2022). https://revisor.mo.gov/main/OneSection.aspx?section=456.4-419

4. RSMo § 456.8-808, Directed Trust and Trust Protector Provisions. https://revisor.mo.gov/main/OneSection.aspx?section=456.8-808

5. Steve Oshins, Dynasty Trust State Rankings Chart (Updated January 2025), Oshins & Associates, LLC. https://www.oshins.com/_files/ugd/b211fb_a6190c927f7c4feb92d5a40835cf243a.pdf

6. Steve Oshins, 11th Annual Domestic Asset Protection Trust State Rankings Chart, Oshins & Associates, LLC: https://www.oshins.com/_files/ugd/b211fb_e159190aa9c04112af068c994dc2c144.pdf

7. The Missouri Bar — 2025 Legislative Session: Four Missouri Bar-Initiated Trust Provisions. https://news.mobar.org/four-missouri-bar-initiated-provisions-pass-through-missouri-general-assembly/