INVESTMENT MANAGEMENT

SpaceX Unpacked

JUNE 5, 2026

Key Takeaways:

- SpaceX is Going Public — On June 12 at a $1.77 trillion valuation — the largest IPO in history — SpaceX is going public. What investors are actually buying is a four-business conglomerate spanning rockets, satellite internet, frontier AI, and social media, priced at 95× trailing revenue with widening losses.

- Whether You Participate or Not, You Will Likely Own SpaceX Soon — Index providers have rewritten their rules to fast-track inclusion, and analysts estimate index funds will absorb nearly a quarter of SpaceX’s public float within six months.

- Musk Retains 82.4% of the Voting Power — Insiders are locked into a staggered six-month selling schedule tied to earnings events the company has never had to deliver publicly, and the academic record on mega-IPO performance is unkind. Investors considering participation should understand they are underwriting a founder, not a spreadsheet.

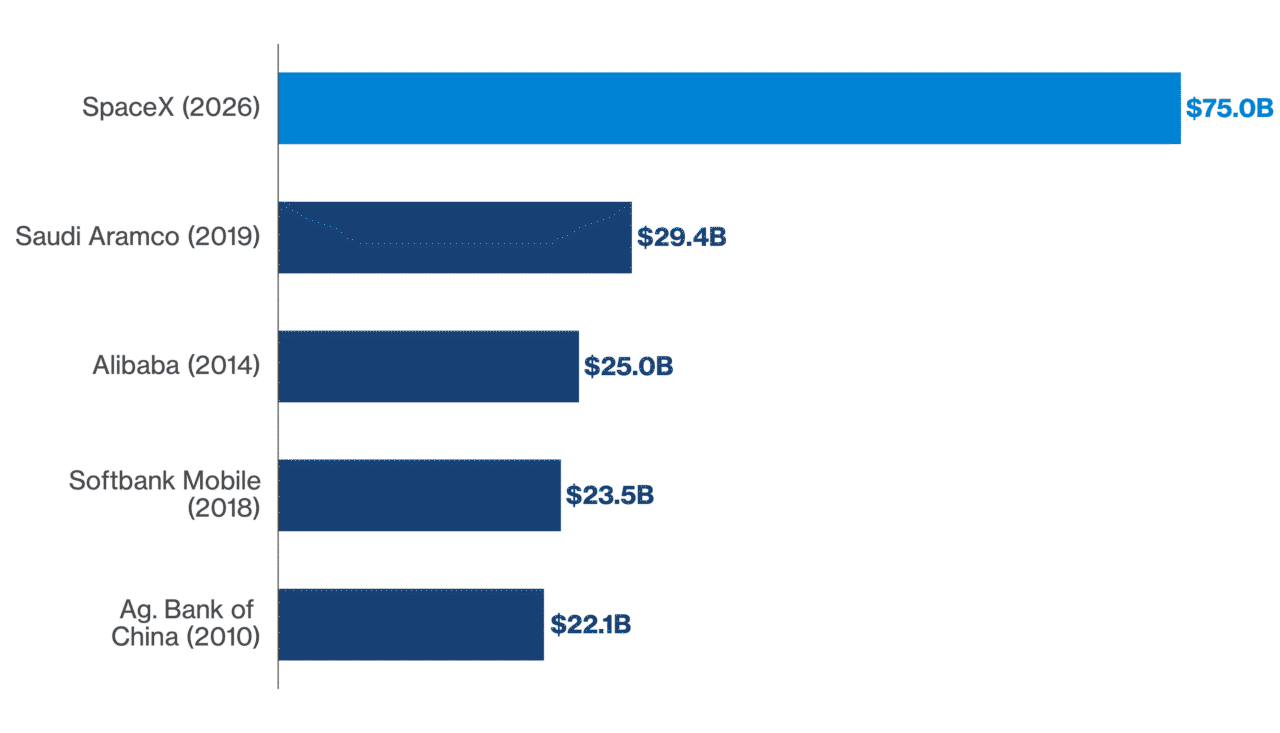

SpaceX’s IPO breaks the mold on nearly every dimension. The company set the price before the roadshow, allocated an unusually large share to retail investors, replaced the conventional lockup with a staggered release, and persuaded major index providers to rewrite their inclusion rules. SpaceX’s June 4th filing priced its IPO at $135 per share, offering 555.6 million shares for a $75 billion raise, at a valuation of approximately $1.77 trillion.

That’s 2.5 times the previous largest IPO in history, Saudi Aramco, and would make SpaceX the 7th most valuable publicly traded company on day one.

SpaceX is a Conglomerate

This is far from the pure-play space company many assume. Since the February 2026 xAI merger, SpaceX has operated as a conglomerate spanning four distinct businesses:

- Rockets and launch services,

- Satellite internet,

- Frontier AI infrastructure, and

- A social media platform (x.com, formerly Twitter)

Starlink is the Current Profitability Engine

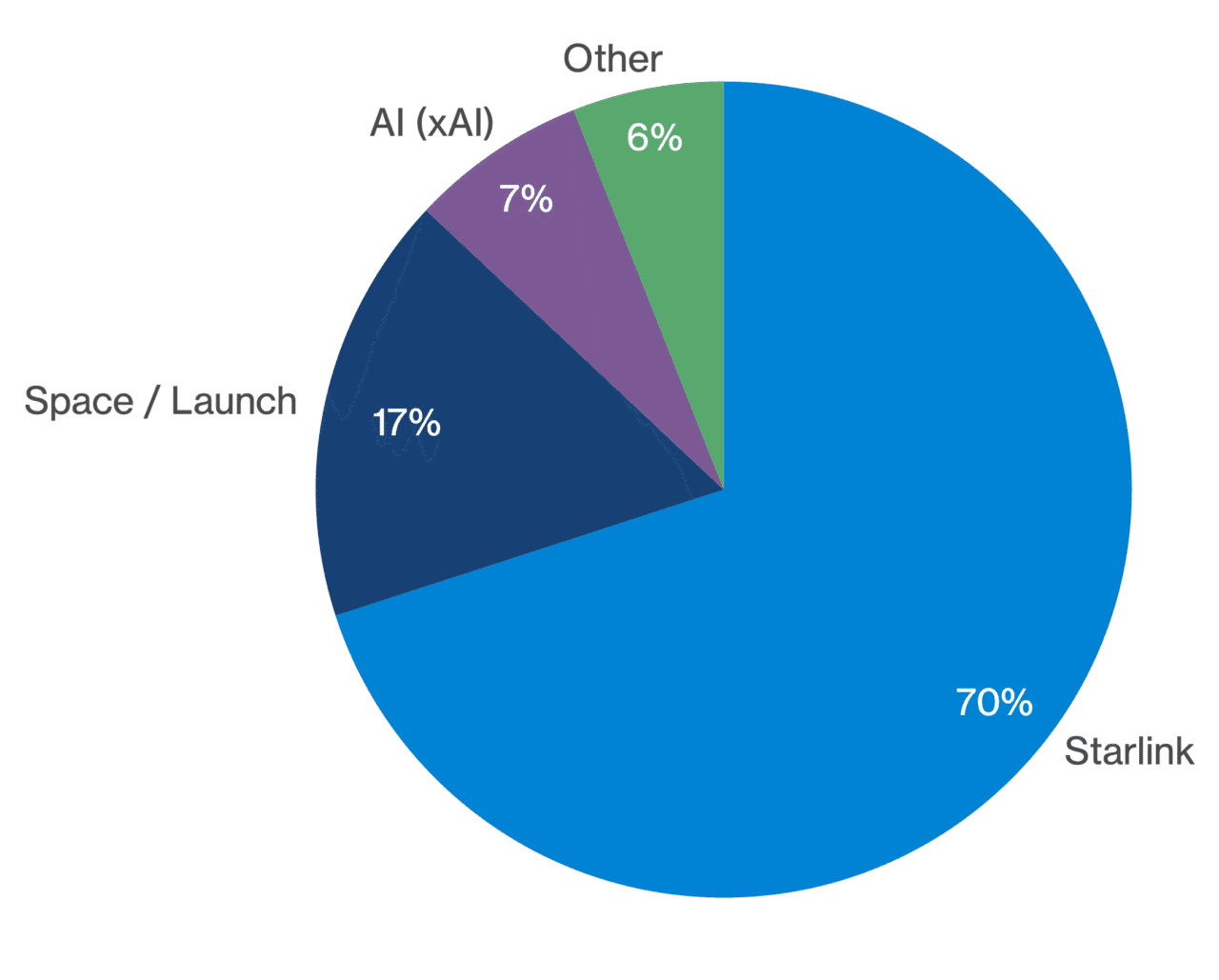

The S-1 offers the first public look at the financials, and the picture is messier than the rocket-company narrative suggested. SpaceX generated $18.67 billion in 2025 revenue, up 33% year-over-year, but posted a $4.9 billion net loss. Starlink drives cash flow, contributing nearly 70% of firmwide revenue and delivering cushy 63% EBITDA margins that resemble a software company more than a satellite operator.

Breakdown of SpaceX 2025 Revenue by Segment

The U.S. government is SpaceX’s single largest customer, accounting for more than 20% of total revenue from Starlink connectivity contracts, classified Starshield work (SpaceX’s government-focused satellite network and services program), and national security launch services. That relationship is both a floor and a ceiling. While SpaceX provides durable, mission-critical demand that no commercial competitor can easily displace, it also ties a meaningful share of its revenue to budget cycles, political dynamics, and the scrutiny that accompanies government contracting.

Questions About xAI

The AI segment is perhaps the least understood part of the business. SpaceX’s xAI subsidiary operates Grok and runs one of the world’s largest GPU clusters (GPUs are the specialized chips that train and run AI models; owning a massive cluster of them is the AI equivalent of owning the power plant, not just the electricity).

Its single largest customer is Anthropic, a direct competitor, which pays $1.25 billion per month for access to xAI’s infrastructure, subject to a 90-day termination clause. The contract confirms the infrastructure is real but raises two harder questions: why is xAI sitting on this much excess capacity, and how durable is roughly $15 billion in revenue when either side can walk away on short notice?

Is SpaceX Worth $1.77 Trillion?

At a $1.77 trillion valuation on $18.67 billion in revenue, SpaceX is priced at roughly 95× trailing sales, a multiple that exceeds every member of the Mag 7 today. The company is not yet profitable. For context, Morningstar’s discounted cash flow model arrived at a fair value of $780 billion; PitchBook’s independent analysis placed fair value between $1.1 and $1.7 trillion. The range of credible institutional views is wide, and the IPO price sits at or above the top end of it.

Musk Retains Control of SpaceX

Musk retains 82.4% of the voting power through a dual-class structure, making SpaceX a Nasdaq “controlled company” exempt from governance requirements that most investors take for granted: majority-independent boards, independent compensation committees, and independent director nominations. Investors in SPCX are buying an economic interest in the business, not a voice in how it’s run.

This IPO is an all-primary offering, meaning 100% of the proceeds go to the company, and no insiders are selling at the IPO. Read that two ways: insiders believe the stock is worth more than $135, and SpaceX needs the money — $20 billion in a bridge loan due in 15 months and a cash-intensive buildout of AI infrastructure — and Starship doesn’t fund itself.

SpaceX Will Be Fast-Tracked into Indices

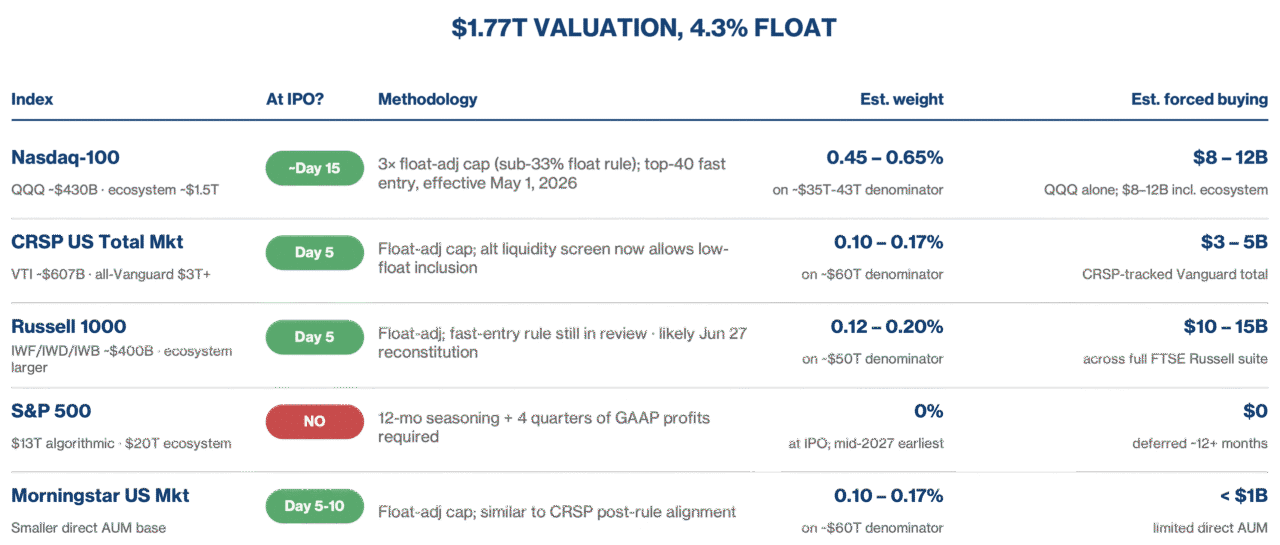

A consequential development, and the one most investors have overlooked, is that the index providers have rewritten their rules to accommodate SpaceX.

NASDAQ introduced a “Fast Entry” rule effective May 1, allowing any company ranked in the top 40 by market capitalization to enter the NASDAQ-100 after just 15 trading days. Previously, new listings were subject to a 3-month waiting period before inclusion in the index. NASDAQ is also waiving the minimum free float requirement of 10% and allowing SpaceX to be included in the index, even though only 4.3% of its shares will be publicly traded. Additionally, NASDAQ will apply a 3x multiplier to its weighting calculation, so SpaceX is weighted as though roughly 12.9% of its shares were public rather than 4.3%, inflating its benchmark weight.

FTSE Russell has similarly compressed its typical timeline, allowing SpaceX to be included in the Russell 1000 Index after as few as five trading sessions. Under the prior rule, IPOs had to undergo a quarterly review and maintain a minimum float of 5% before being included in the index.

S&P 500 was considering shortening its “seasoning period” (the 12-month waiting period newly listed companies must undergo after going public) to six months and waiving the profitability requirement for mega-cap companies. After deliberation and in a “wild twist,” S&P has decided not to change its rules to allow SpaceX’s early inclusion in the index.

Note: Nasdaq-100’s 3× float multiplier (sub-33% float rule) is the big boost. Without it, SpaceX would weigh ~0.10% in QQQ, which is roughly the same as a mid-cap straggler. S&P 500 confirmed absence (decision finalized June 4, 2026) defers an estimated ~$14B of forced passive buying and creates a temporary benchmark distortion for actively managed mandates. Weight and forced-buying figures are third-party estimates and model-dependent.

Sources: Morningstar, etf.com, FTSE Russell,

https://www.msci.com/research-and-insights/blog-post/how-megacap-ipos-in-2026-could-reshape-global-benchmarks

Analysts estimate that index funds will absorb nearly a quarter of SpaceX’s public float within six months. Any investor who holds a total market index fund or a direct indexing strategy will eventually own SpaceX; the questions are when and at what weighting.

SpaceX is Utilizing a Staggered Lockup

SpaceX also has a unique lockup structure that adds another layer of complexity. It has replaced the typical 180-day lockup with a staggered, performance-driven release of shares for private stockholders.

Musk and a few other key investors are ineligible to sell any shares for 366 days from the IPO.

But after the Q2 earnings call in August, insiders may sell up to 20% of eligible shares (30% is eligible if the stock trades at or above 30% above the IPO price). From there, 7% tranches are released on days 70, 90, 105, 120, and 135. Another 28% unlocks at Q3 earnings, and the remainder unlocks after 180 days.

SpaceX Insider Lockup Waterfall (Staggered Release Schedule)

This staggered liquidity means that insider supply will not arrive in a single December cliff. Rather, it will trickle in over the back half of 2026, with the largest tranches tied to earnings events. Thus, there will be six months of rolling selling pressure from pre-IPO shareholders, rather than the usual sudden pressure from a cliff lockup.

History Shows Mega-IPOs Generally Underperform

The academic record on mega-IPO performance is unkind — Professor Jay Ritter’s long-running work shows IPOs underperforming size– and style-matched peers by about 2% annually over five years, with drawdowns historically clustering around lockup expirations. A single cliff concentrates that pain into one event; a staggered structure spreads it across months of rolling pressure points, each tied to earnings reports the company has never had to deliver as a public filer.

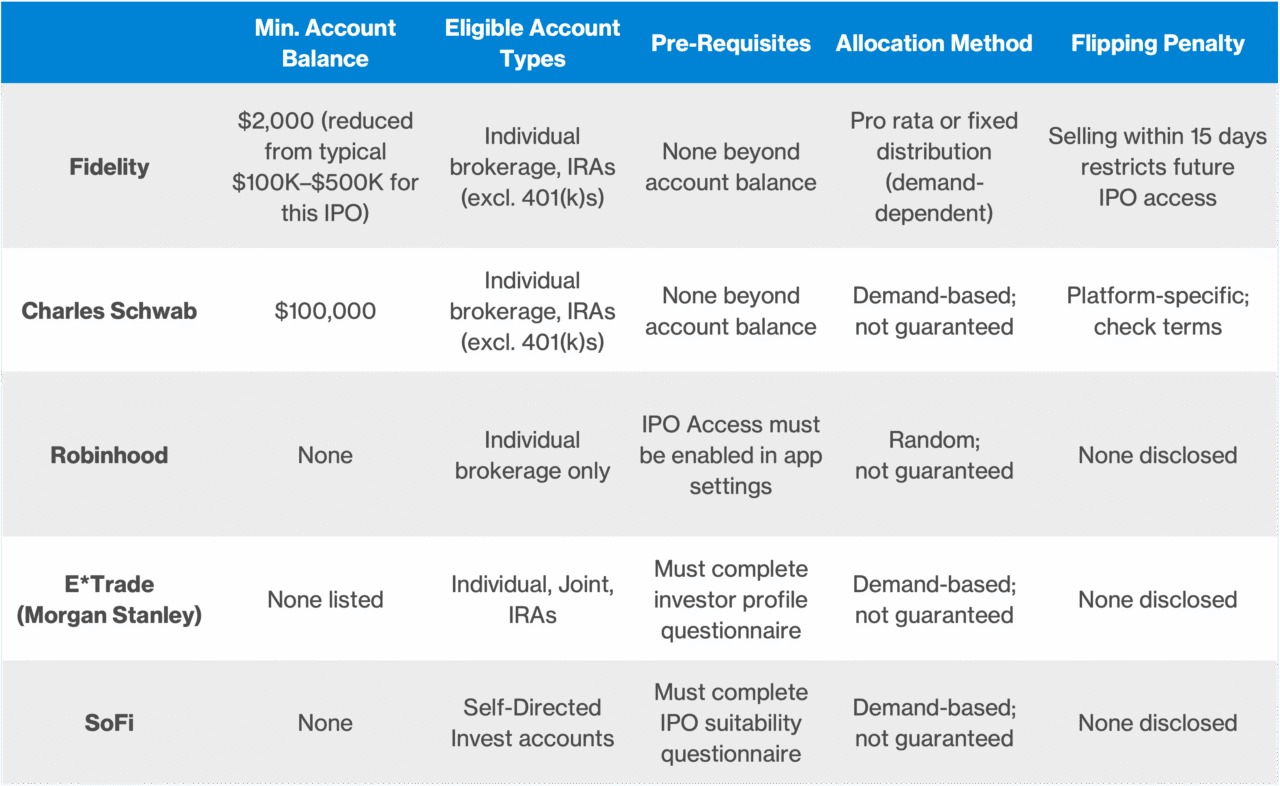

Adding further complexity and likely volatility, Musk has reserved 30% of the offering for retail access through a handful of custodial relationships. Each has different requirements, and several custodians have changed their terms specifically for this IPO.

Where This Leaves Us

This is no ordinary IPO. The offering’s structure, the staggered liquidity, the compressed index-inclusion timelines, the fact that the public shares represent less than 5% of the company, and the conglomerate nature of the business all combine into something the public markets have not had to digest before.

We told our clients earlier this year to expect a significant structural impact on the markets. The shape of that impact won’t be clear until trading begins, but we are tracking it closely through the open.

At 95x trailing revenue with widening losses, the valuation reflects a bet on Elon Musk’s ability to execute a vision that current financials do not yet support. Investors considering participation in the IPO should clearly understand that distinction: they are underwriting a founder, not a spreadsheet.

Sources: SpaceX S-1 and S-1/A (SEC EDGAR, May–June 2026); PitchBook; Morningstar; Bloomberg; Reuters; CNBC; Yahoo Finance; Forbes; ETF.com; Acadian Asset Management; Fidelity; Charles Schwab; Robinhood; E*Trade; SoFi; Forge Global; Hiive; Nasdaq Private Market; Polymarket; Avantis Investors; University of Florida (Ritter IPO data). Information current as of June 4, 2026, 11:00 AM CT. This communication is for informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any security. ArchBridge Family Office is a Missouri state-chartered trust company. Clients should consult their advisor before making any investment decisions