Stablecoins Reach a Legislative Milestone, but Should Investors Care?

Key Takeaways:

-

The GENIUS Act Brings Regulatory Clarity to Stablecoins – By establishing federal oversight, mandating 1:1 reserves in high-quality assets, and requiring audits and anti-money laundering measures, the GENIUS ACT marks a significant step toward legitimizing the sector.

-

Stablecoins Offer Efficiency and Speed in Transactions – Stablecoins operate on blockchain infrastructure outside traditional banking systems, with usage growing to rival established payment networks like Visa in transaction volume.

-

Stablecoins Are Not Investment Vehicles – Their value is designed to remain stable, they pay no interest, and their primary role is to enhance financial infrastructure rather than generate returns for individual investors.

First off, I hope everyone enjoyed Crypto Week. And what a week it was! On July 18th, the Guaranteed and Enhanced National Use of Stablecoins Act, better known as the GENIUS Act, was signed into law by President Trump. This bipartisan legislation establishes a federal regulatory framework for stablecoins, which are digital tokens designed to maintain a stable value.

The act:

- Introduces oversight by the Federal Reserve and other banking agencies,

- Requires a 1:1 reserve requirement in high-quality liquid assets (e.g., U.S. dollars),

- Mandates anti-money laundering (AML) programs,

- Sets clear standards for issuers,

- Prohibits interest payments, and

- Requires regular independent audits.

The GENIUS Act is a celebratory development for the crypto industry, as it brings legitimacy to a market often seen as opaque and speculative. With regulatory clarity now in place, it’s worth stepping back to better understand what stablecoins are, how they function, and whether they have a role in an investor’s portfolio.

What are Stablecoins Anyway?

Stablecoins are a type of cryptocurrency whose value is designed to be stable, typically by being pegged to a traditional currency, such as the U.S. Dollar. They are a programmable, blockchain-based version of money that enables faster and more efficient transactions than those in fiat currency. Plus, stablecoin transactions operate outside of traditional banking infrastructure and beyond traditional banking hours

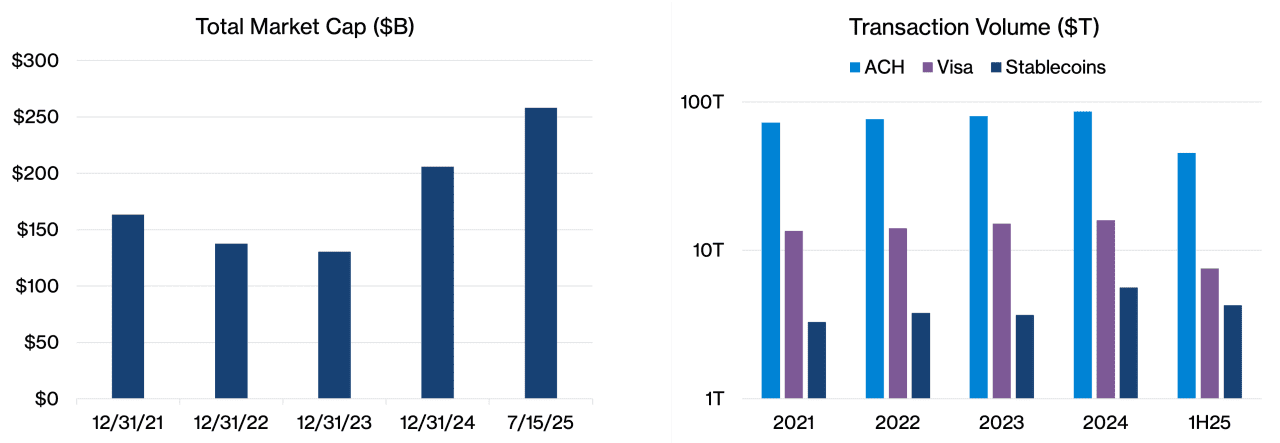

The charts below show the market capitalization of stablecoins and the transaction volume ($) they’ve seen compared to more traditional forms of payment networks, represented by ACH (an electronic payment network in the U.S. that enables banks to transfer funds between accounts) and Visa (a global payments platform).

While the supply of stablecoins in circulation remains modest, their transaction volume is approaching the global payments and cash volumes processed by Visa.

Should I Invest in Stablecoins?

The primary appeal of stablecoins lies in their utility within the financial system rather than their potential as a standalone investment. The infrastructure built for accepting, sending, and transacting with dollars has been developed over decades. Still, it has limitations, costs, and inefficiencies (these issues are apparent to anyone who has sent a wire transfer!).

Financial institutions, such as JP Morgan, Bank of America, and Citigroup, are exploring the use of stablecoins to facilitate near-instant settlement of trades, enable global remittances, and streamline cross-border payments. Large tech and payment companies, such as Stripe, Amazon, Uber, Meta, and Apple, are investigating stablecoins (likely by creating their own) to unlock cost savings and streamline payments at scale. Fintech companies view them as an access point to decentralized finance (DeFi) applications. Because of their stability and blockchain-native format, they serve as a bridge between traditional finance and digital innovation. For now, their use is primarily behind-the-scenes, mainly powering digital asset platforms, payment rails, and financial infrastructure, rather than being a tool for everyday consumer spending.

While stablecoins represent a significant technological advancement – and now one formally recognized due to the GENIUS Act – they function more like a currency than an investment opportunity. Their value does not appreciate, they don’t pay interest, and their role is to mirror the dollar, not outperform it. Thus, there is little reason to consider allocating to stablecoins within a portfolio. Instead, their development serves as a reminder that innovation continues to reshape the financial plumbing. The real beneficiaries may be the platforms and firms that adopt the technology early – not individual investors seeking returns.